Cash Flow Planning: Expenditure and Dealing with Deficits

Having looked at income, we now turn to expenditure. Here, there is tends to be more certainty, especially with regard to fixed costs (the costs we incur whether or not we have any work). For example, we know what rent or rates we are going to pay. We know what our utility bills are going to be. We know how much we’re paying for our phone. All of these tend to be regular payments that can be entered into the monthly columns.

Of course, if we are working from home and charging a proportion of the household costs to the business, we can choose to do this annually rather than monthly — or even to waive the charge altogether until the business is established. But if we do this, we have to remember we are giving ourselves a false picture when assessing how successful we have been.

The variable costs (those associated with a particular piece of work) are a little more difficult but for each income figure we enter, we should be able to estimate the related costs. These need to be entered at the time they are incurred (or at least paid for) which will often be before the income arrives.

To finish the statement, we need an opening balance for the beginning of the year and a carried forward figure at the end of each period (month). Remember that we do not start each month afresh. If we have a deficit at the end of one month, that is the opening balance at start of the next month.

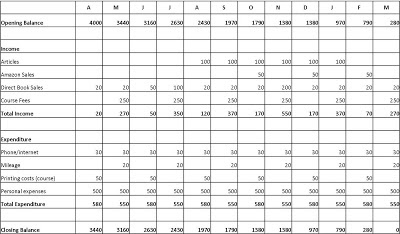

OK, I think it is now time for a picture, or at least a chart. Let’s have a look at an example (and remember, the only purpose of these numbers is to illustrate the points, so we shouldn’t get hung up on whether they make sense individually or not).Example 1 (click on chart to enlarge)

In this example, we have the four different income streams: six articles paid monthly between August and January; Amazon sales which come in bimonthly from October onwards; direct sales to the public which vary depending on events per month; and fees for running a writing course every two months. We see that the income varies between £20 and £370 per month.

For expenditure, we have a regular monthly contract for phone and internet; we have mileage costs and printing costs associated with the course, the former occurring in the same month and the latter a month earlier in each case; and we have a regular ‘drawing’ to cover our personal expenses. Whether this is a salary that we are paid as an employee of a limited company, or whether it is a drawing we make as a sole trader is irrelevant here. This is the money we need to live (and again – these are examples only, not real figures). We see that our total expenditure is fairly fixed at between £550 and £580 per month.

We have started the year with an opening balance (i.e. funding) of £4000. At the end of the year, our closing balance is zero. This means that we are projecting a loss of £4000 during the year. But remember, we are talking here about cash flow. What this tells us is that if we start with £4000, we will have enough cash to last the year but that we will need to sort out more funding (or raise income, or reduce expenditure) at the beginning of the next financial year.

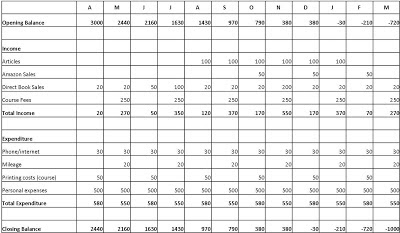

Let’s suppose we don’t have a £4000 pot to start the year off. What happens if we only have £3000?Example 2 (click on chart to enlarge)

In this case, our cash flow goes negative in December and we need to find more funding at that point but we have demonstrated that we can start with a smaller pot and keep the business running.

If we have our cash flow set up in a spread sheet, as I’ve shown here, it’s very easy to play the ‘what if’ game by changing some of the figures and seeing what the effect is on the bottom line. For example, try pushing up the income or reducing the expenditure to see what happens. This is also useful for crystallising exactly what we need to do to make the business a success.

As always, note that I am not an accountant or a lawyer, just a long-term business owner, talking about my own experience. If you are unsure about anything, always take advice from an appropriate professional.

Comments (1)